Why Generate

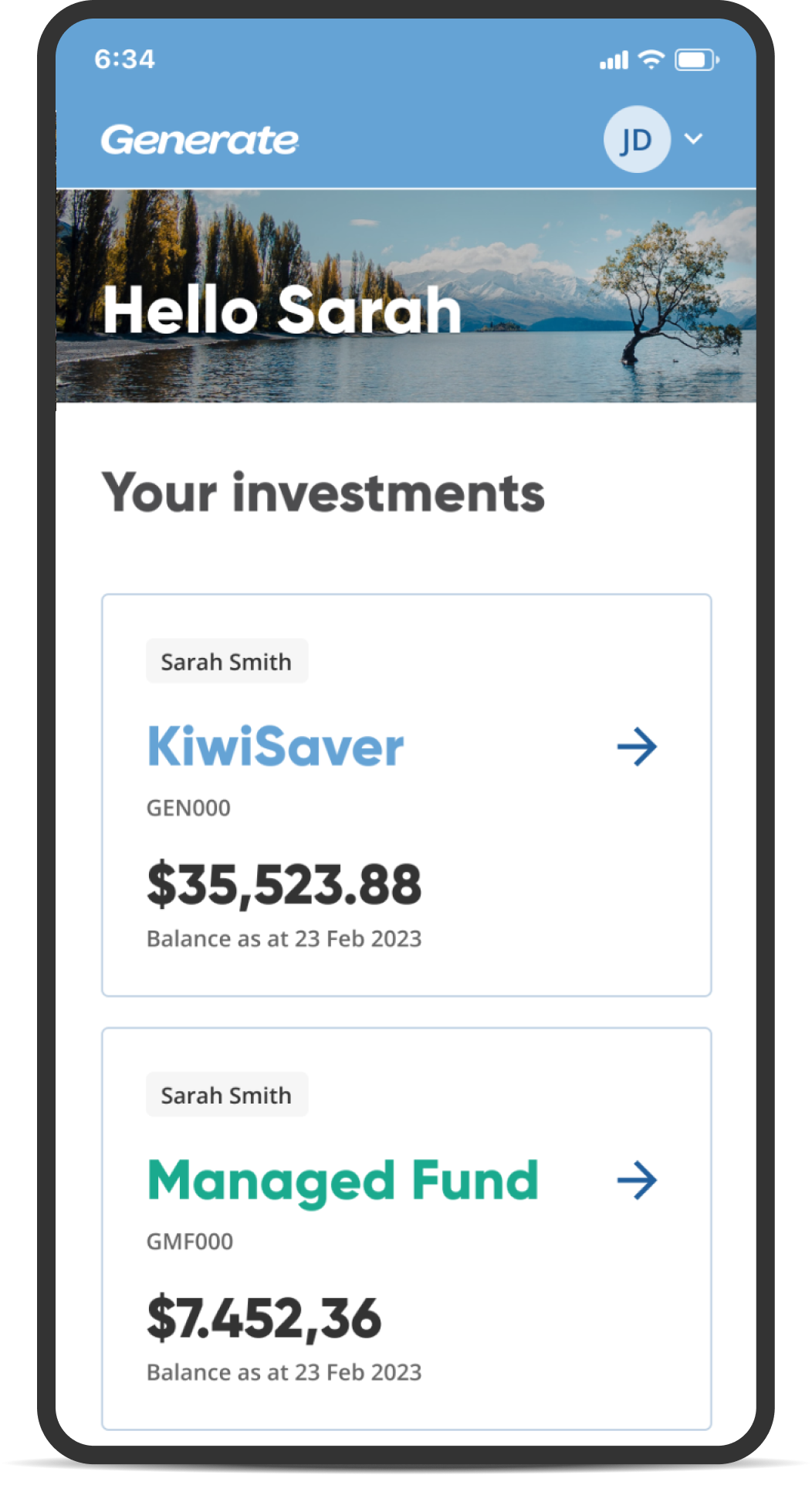

KiwiSaver

Managed Funds

Resources

Contact Us

Join Generate KiwiSaver

Join or switch online now in five minutes

Join Generate Managed Funds

Get started investing within ten minutes

Member login

Adviser login

Generate accounts, Scheme management, risks and Anti-Money Laundering...

Voluntary contributions, employers contributions, overseas payments...

ID and proof of address certification, under 18s, self employment...

Significant financial hardship, serious illness and emigration withdrawal...

KiwiSaver and Managed Fund fees, Scheme taxes...

Feedback, contact, experience with Generate, complaints...

Login, download the new app, forgot password, tax certificate...

Difference between Managed Funds and KiwiSaver, applying for a Managed Fund, withdrawal...